{kind=link}

I created this piece to expand on a short, direct message I shared on compliance best practices for agents who sell Small Business Health insurance, Medicare, ACA plans, and life coverage. As the person who has been in the trenches, I want to give you clear, practical guidance because compliance is not optional — it’s the backbone of a sustainable practice. In this article I walk through why recording calls matters, how to handle language barriers, what to document, how to respond to inquiries, and how to build a long-term Small Business Health insurance book that keeps paying month after month.

Table of Contents

- Why compliance is non-negotiable 🚨

- How to handle language barriers and interpreters 🗣️

- Recording calls: best practices and what to say 📞

- Dealing with inquiries and appeals 📝

- Building a long-term Small Business Health insurance practice 🧭

- Practical checklist: daily workflows for compliance ✅

- Common mistakes agents make and how to avoid them ⚠️

- FAQ 🤔

- Next steps and call to action 💪

Why compliance is non-negotiable 🚨

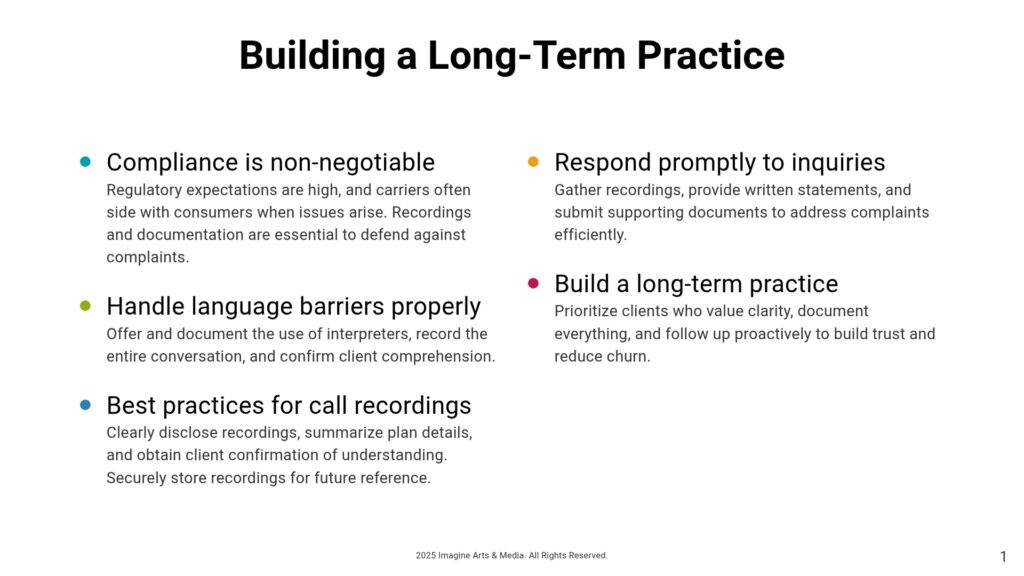

If you sell Small Business Health insurance, Medicare, ACA plans, or life insurance, compliance is the thing that will make or break your career. I can’t stress this enough: regulatory expectations are high, and carriers usually side with the consumer first when something goes wrong. I learned early on that when a policyholder rings the carrier and reports a problem, the carrier’s first instinct is to support the member — not the agent.

That means you must have proof. The clearest, most defensible proof you can have is a recorded call with clear disclosure that the call is being recorded and documentation that the client understood the plan limitations and benefits. If you don’t have that, you will spend hours answering inquiries, writing letters, and possibly facing investigations that could threaten your license.

“Insurance companies are going to first favor the client.”

That quote isn’t alarmist — it’s reality. When a member says, “I couldn’t use my card at the pharmacy,” or “this drug wasn’t covered,” carriers open cases. The member’s story is the starting point. Your recorded evidence and file notes determine whether the carrier accepts the agent’s explanation or opens an investigation. If you sell Small Business Health insurance without rigorous documentation, you’re taking on risk you might not be prepared for.

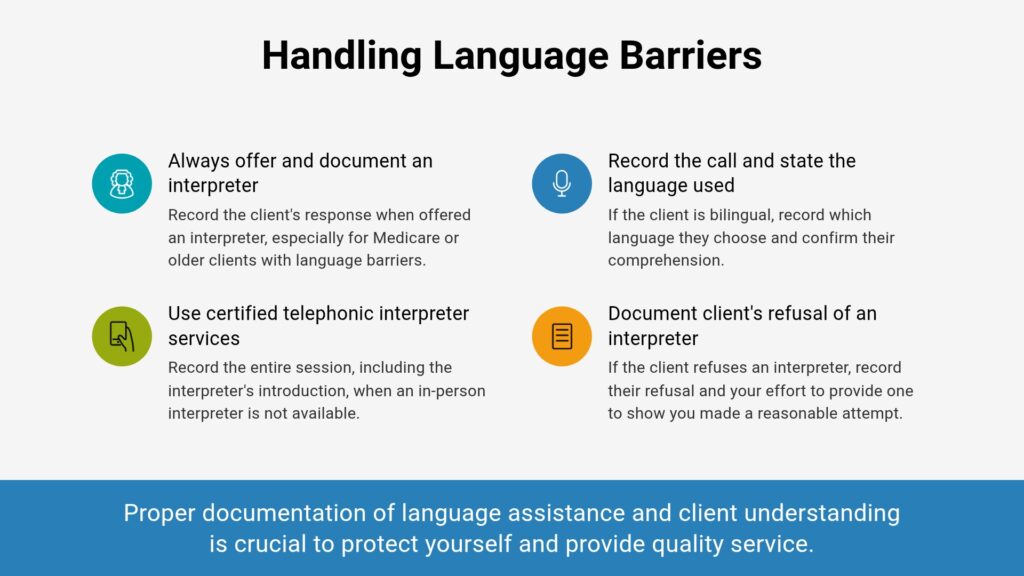

How to handle language barriers and interpreters 🗣️

One of the biggest sources of risk I see is language mismatch. When a client doesn’t fully understand English — and you don’t speak their language fluently — misunderstandings happen fast. This is especially true with Medicare clients and older members who may have hearing or cognitive issues.

Here’s what I do and recommend you do every time:

- Always offer and document an interpreter when there’s any language barrier. I say, “Would you like an interpreter?” and record their answer.

- Use certified telephonic interpreter services if an in-person interpreter is not available. Record the entire session, including the interpreter introduction.

- Record the call and explicitly state the language being used. If the client is bilingual, record which language the client chooses and confirm comprehension.

- If the client refuses an interpreter, record that refusal and your effort to provide one. Your documentation should show you made a reasonable attempt to ensure understanding.

These steps protect you. When compliance asks if the client understood the plan’s formulary or prior authorization requirements, you can point to the recorded interaction and the documented offer of an interpreter. That level of documentation often prevents misunderstandings from escalating into formal complaints.

Recording calls: best practices and what to say 📞

Recording calls is not just about hitting a button. There are specific things I always include in my calls to create a defensible file.

Start the call with a clear disclosure and confirmation:

- State plainly: “This call is being recorded for quality and compliance purposes. Do I have your consent to continue?”

- Note the time, agent name, client name, and the purpose of the call at the top of your file or CRM entry.

- Summarize the plan highlights and exclusions in plain language, and then ask the client to repeat in their own words what they understood. Record that exchange.

- If discussing drugs or prior authorizations, explicitly name the key drugs the client takes and confirm whether they are included or excluded from the plan formulary.

Why this matters: Inquiries often stem from the member reaching the pharmacy and discovering a drug is not covered. If you documented that conversation and obtained confirmation that the member understood, you typically have the evidence to show you fulfilled your duty of explanation.

Store recordings securely and tag them clearly in your CRM by date, client, and policy type. I recommend keeping them for the period required by your carrier and state regulation — but also long enough to support any future investigations. Don’t assume “the carrier will remember.” Documentation wins disputes.

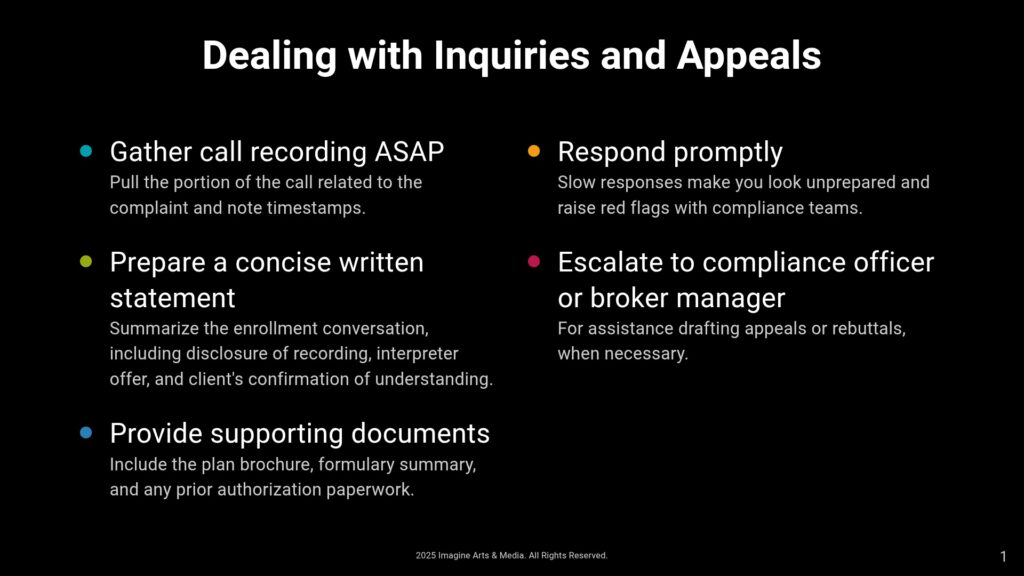

Dealing with inquiries and appeals 📝

Even with perfect documentation, inquiries happen. Clients get frustrated; pharmacy interactions go badly; providers misinterpret coverage. When a carrier opens an inquiry and names you as the agent on record, here are the steps I take and recommend:

- Gather the call recording ASAP. Pull the portion of the call related to the complaint and note timestamps.

- Prepare a concise written statement summarizing the enrollment conversation, including the disclosure of recording, interpreter offer, and the client’s confirmation of understanding.

- Provide supporting documents: the plan brochure, formulary summary, and any prior authorization paperwork, if applicable.

- Respond promptly. Slow responses make you look unprepared and raise red flags with compliance teams.

- When necessary, escalate to a compliance officer or broker manager for assistance drafting appeals or rebuttals.

I’ll be honest: responding to inquiries is a pain. It’s time-consuming, stressful, and at times discouraging. I’ve seen many agents think, “This isn’t worth it. I’ll walk away.” But if you want a long-term business around Small Business Health insurance, you need to accept inquiry work as part of the job and build systems to make it manageable.

Building a long-term Small Business Health insurance practice 🧭

This is a long-game industry. If you’re looking for quick wins, you’ll burn out. If you want recurring commissions and steady income, you must treat compliance and client understanding as investments in your future book of business.

Here’s how I build portfolios of proper clients and why it works:

- I prioritize clients who are willing to do the paperwork and who value clarity over price alone.

- I take a consultative approach: explain trade-offs in plain language, discuss drug formularies, prior authorization requirements, and network limitations up front.

- I document everything, so renewals and cross-sells are smooth and defensible.

- I follow up proactively after enrollment — a short recorded check-in at 30 days can prevent many complaints from escalating.

Making these adjustments in how you sell Small Business Health insurance creates trust, reduces churn, and increases the likelihood of referral and retention. Commissions that feel small in the short term compound into reliable income as your client base grows.

Practical checklist: daily workflows for compliance ✅

To make compliance habitual rather than burdensome, I use a daily and per-enrollment checklist. You can adapt this to any CRM or process tool you use.

- Before the call: pull client file, list key meds and providers if provided, prepare to offer interpreter services.

- At start of call: disclose recording and consent, confirm client identity and contact details, note language preference.

- During the call: cover plan highlights, exclusions, formulary items, prior authorization steps; request client to summarize in their words.

- After the call: tag and save the recording with date, time, and a short summary; upload any forms, screenshots, or emails to the client file.

- Follow-up: 7–14 days after enrollment, do a brief recorded check-in to make sure claims or pharmacy issues haven’t started.

- Annual review: before renewal season, confirm changes in medications and providers and document any shift that might affect plan suitability.

Common mistakes agents make and how to avoid them ⚠️

I’ve seen a lot of agents get tripped up by the same issues. Here are the most frequent mistakes and my solutions:

- Assuming understanding: Agents often assume the member “got it.” Always get verbal confirmation and, when appropriate, ask the member to restate the important points.

- Skipping recording disclosures: If you forget to record or don’t announce it, you have no proof. Make the disclosure part of your opening script.

- Poor documentation of interpreter usage: If language is an issue, document your interpreter offer and the client’s response. Use telephonic interpreters when needed and record the entire exchange.

- Failing to list medications: Not checking a client’s key prescriptions at enrollment is a major cause of future complaints. Ask and document specific drugs and whether they were on the formulary.

- Slow response to inquiries: When compliance calls, act fast. Delays look bad and can escalate matters unnecessarily.

By eliminating these mistakes, you not only reduce your risk but also offer higher-quality service to your clients. That reputation becomes an asset when you’re building a book of Small Business Health insurance clients.

FAQ 🤔

Q: Do I always have to record calls when selling Small Business Health insurance?

A: In most cases, yes. Recording calls is essential when selling Medicare, ACA, or employer-sponsored Small Business Health insurance, especially if the carrier or state requires it. Even if it’s not explicitly required in your state, recording is a best practice that protects you and your client. I record every enrollment call and any call involving plan explanations or appeals.

Q: What should I say at the start of a recorded call?

A: A good script keeps it simple and clear: “Good morning, this is [Your Name] from [Agency]. This call is being recorded for quality and compliance. Is that okay?” After the client confirms, say the purpose of the call and record the full conversation. If you need to tailor language for the hearing impaired or for non-native speakers, do so and document the accommodation.

Q: How long should I store recordings for Small Business Health insurance enrollments?

A: Follow your carrier and state retention policies — often that’s several years. I store recordings for at least the timeframe the carrier recommends and keep critical files longer when there are active claims or potential inquiries. Secure storage with controlled access is essential.

Q: What do carriers typically ask for during an inquiry?

A: Expect requests for the recorded call, a written agent statement, enrollment documents, evidence of prior authorization requests, and any other supporting forms. Be ready to provide a concise timeline and the exact portion of the call relevant to the inquiry.

Q: Can I refuse to enroll someone who refuses an interpreter when language is a barrier?

A: You must use professional judgment. If the client refuses an interpreter but you have reasonable belief they do not understand the plan, document your concerns and the client’s refusal. If it’s unsafe to proceed, you should pause the enrollment until the client agrees to an interpreter. Protecting the client and yourself is the priority.

Q: How does this affect my Small Business Health insurance renewals?

A: Good documentation makes renewals smoother. If you have clear records about the client’s needs and decisions, you can make accurate recommendations year after year. That reliability increases retention and your lifetime value per client.

Next steps and call to action 💪

If you’re serious about building a sustainable Small Business Health insurance practice, start by tightening your enrollment process today. Implement a script that includes recording disclosure, interpreter offers, and medication confirmations. Save and tag your recordings, then schedule routine follow-ups. These habits take time to develop, but they’re the difference between playing the short game and building a long-term business.

If you’ve encountered a situation where compliance became a headache — or you need help crafting scripts, checklists, or document retention practices — tell me about it in the comments. I’ll share real examples and templates that I use. Building a compliant, profitable Small Business Health insurance book isn’t easy, but it’s achievable with the right systems and discipline.

Remember: Compliance protects your clients and your livelihood. Insurance companies will often favor the client in disputes, so your best defense is clear, consistent documentation — and that starts with recording the call.

Have a great day, and if you want more practical, no-nonsense tips on building a durable Small Business Health insurance practice, let me know how I can help in the comments.

Are you someone which needs help on being a better agent? Click to connect

Are you a small business owner? |

|

I can save you at least 50% or more on your Health insurance via The ACA |

| Connect with me |